On April 11, the General Counsel of the CFPB, Seth Frotman, delivered a speech at the National Consumer Law Center/National Association of Consumer Advocates Spring Training, highlighting how the FDCPA and the FCRA cover often-overlooked sectors of consumer finance, including medical collections and landlord-tenant debts. As to medical billing, collections, and credit reporting, Frotman noted that the CFPB has received more than 15,000 complaints in the past two years, as explained previously in the CFPB’s most recent FDCPA annual report (covered by InfoBytes here). These complaints led to the CFPB initiating a rulemaking process to “remove medical bills from credit reports.” Frotman highlighted that many states have taken similar initiatives: Colorado and New York both enacted laws prohibiting the reporting of medical debt, and the CFPB encouraged more states to follow their lead; Connecticut recently introduced legislation banning medical debt in SB 395. Of interest, Frotman noted that when the CFPB contacted debt collectors about suspected bills, they often closed the account – suggesting that these collectors “do not have confidence that this money [was] actually owed,” indicating that collectors could be seeking to collect an invalid medical debt from consumers.

On rental collections and credit reporting, Frotman noted an increase in the “financialization” of the landlord and tenant relationship, such as products to finance security deposits or rent and offering rent-specific credit cards. Frotman also noted that corporate landlords, who have increased their share of the rental housing market, have increased the demand for “tenant screening” products that score prospective tenants. Frotman expressed concern that the algorithms relied on by these tenant screening products have been opaque and even discriminatory. The speech highlighted the CFPB’s focus on tenant screening as part of the Bureau’s increased attention toward debt collection and credit reporting companies generally in the rental industry. For instance, the CFPB noted that law firms that operate as “eviction mills” (i.e., firms that “rubber stamp” eviction actions without performing a meaningful review) could be held liable under the FDCPA.

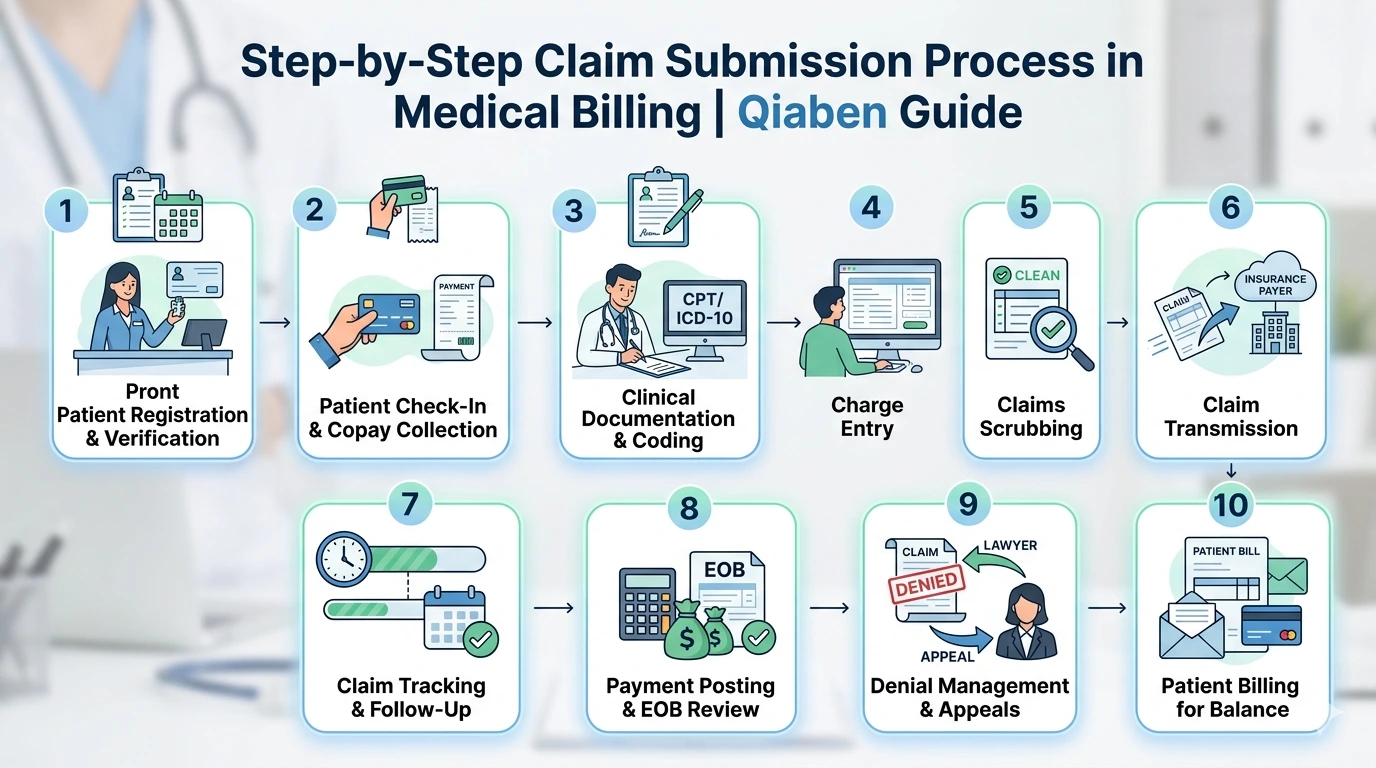

How Qiaben HCS Can Help?

At Qiaben HCS, we offer comprehensive billing services that handle every aspect of the billing cycle. From patient registration and insurance verification to claim submission and follow-up, our professionals ensure that your billing process is efficient and error-free. We focus on maximizing your reimbursement rates and minimizing denials, allowing your dental practice to thrive.

Introduction

Managing medical debt and navigating rental financial products have become growing concerns for millions of Americans. To address these challenges, the Consumer Financial Protection Bureau (CFPB) has taken a closer look at how debt collections and rental products impact consumers. Recently, CFPB’s top consumer advocate, Rohit Chopra and Assistant Director Rohit Chopra’s appointee, Frotman, emphasized the need for transparency, fairness, and better protections. In this blog, we’ll explore what the CFPB’s expert advice means for both consumers and the financial services industry.

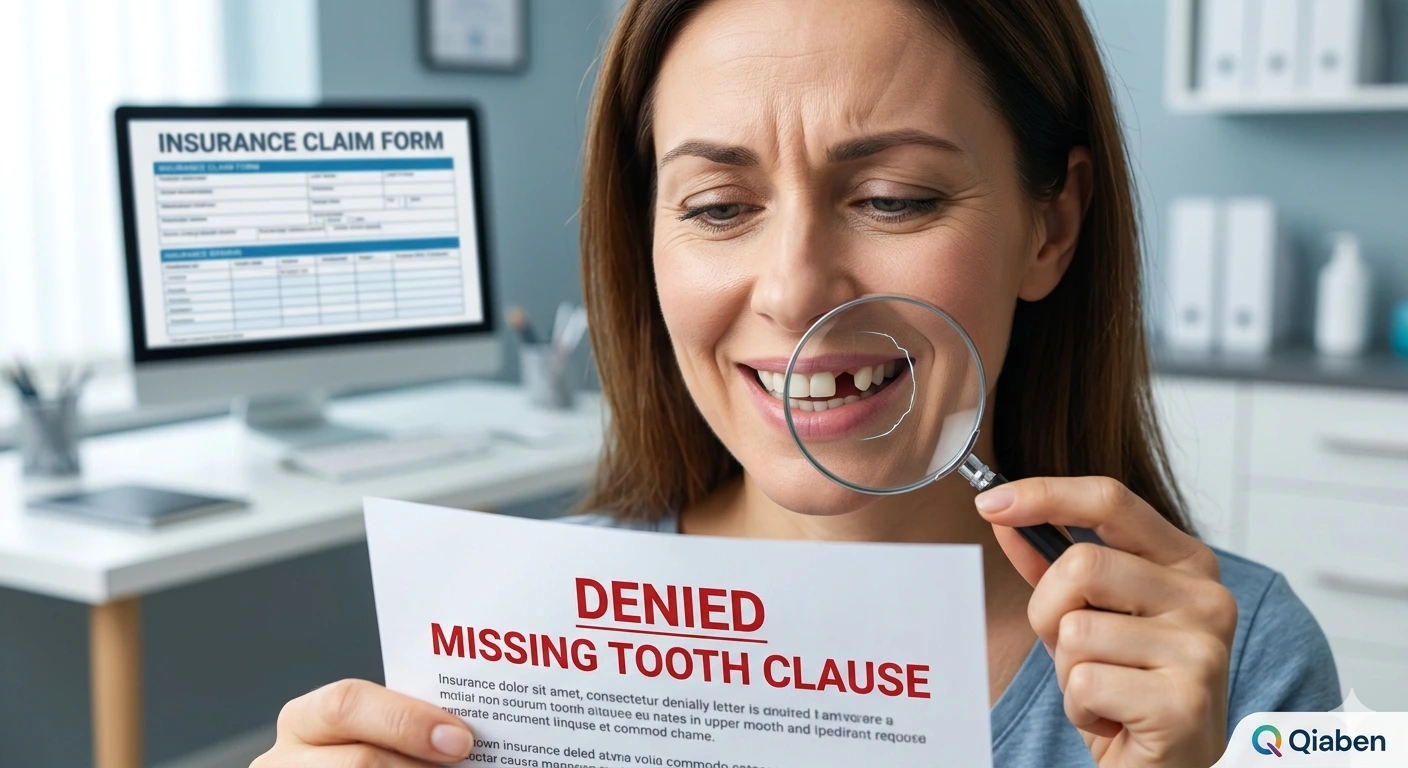

Understanding the Medical Debt Crisis

Medical debt is one of the leading sources of financial stress in the United States. According to CFPB data:

Over 100 million Americans are struggling with some form of medical debt.

Debt collection agencies often use aggressive tactics, putting additional stress on patients.

Medical bills are frequently reported inaccurately on credit reports, damaging consumer credit scores.

CFPB’s stance: The Bureau has made it clear that consumers should not be penalized for medical debt in the same way as other forms of debt. Frotman highlighted that many individuals with medical debt are financially responsible but faced unexpected health crises.

CFPB’s Guidance on Medical Debt Collections

The CFPB advises both patients and providers to focus on transparency and accuracy in medical billing. Here are the key takeaways:

Accuracy in Credit Reporting – Medical debts must be accurately reported to credit bureaus. Errors can unfairly impact creditworthiness.

Clarity in Billing – Hospitals and providers should provide clear, itemized bills so patients understand charges.

Fair Collection Practices – Collection agencies must comply with the Fair Debt Collection Practices Act (FDCPA). Harassment or deceptive practices are prohibited.

Patient Protections – Consumers have the right to dispute debts and request verification before paying collections.

By enforcing these principles, the CFPB aims to reduce financial harm while holding collectors accountable.

Rental Financial Products: An Emerging Concern

Beyond medical debt, the CFPB has started focusing on rental financial products. These include services like:

Rental payment reporting tools that claim to help tenants build credit.

Tenant screening reports used by landlords to evaluate applicants.

Rental deposit alternatives such as security deposit insurance or installment products.

While these products promise convenience, they can also carry hidden fees or risks.

CFPB’s Advice on Rental Finance

Frotman emphasized that renters need greater transparency when dealing with rental financial products. The CFPB highlighted several consumer concerns:

Hidden Fees – Some rental deposit alternatives charge recurring fees, costing tenants more over time.

Credit Impact – Not all rental payment reporting services benefit consumer credit scores, despite marketing claims.

Privacy Risks – Tenant screening companies may mishandle or misreport data, harming rental opportunities.

Discrimination Risks – Inaccurate or biased reports could unfairly disadvantage certain groups of renters.

The CFPB advises renters to carefully review agreements, compare options, and know their rights under federal consumer protection laws.

How Consumers Can Protect Themselves

Based on CFPB’s expert advice, here’s what consumers should keep in mind:

For Medical Debt

Always review medical bills carefully before paying.

Dispute any errors with both the provider and collection agency.

Request a debt validation letter if contacted by collectors.

Monitor your credit report for inaccuracies.

For Rental Financial Products

Read the fine print before signing rental deposit alternatives.

Ask landlords about all available payment options.

Verify whether a rental payment reporting service actually boosts your credit.

Keep records of all rental payments for your protection.

Why CFPB’s Role Matters

The CFPB serves as a watchdog for consumer rights. By spotlighting issues in medical debt collections and rental financial products, the Bureau helps:

Consumers avoid financial pitfalls and protect their credit.

Providers & landlords adopt fairer, more transparent practices.

Policymakers create stronger regulations for financial products.

Ultimately, CFPB’s guidance empowers consumers to make informed financial decisions while pushing the industry toward accountability.

Conclusion

Medical debt and rental financial products are more than just financial concerns—they’re issues that directly impact household stability and long-term economic health. CFPB expert advice encourages consumers to stay informed, challenge unfair practices, and demand transparency.

Whether you’re struggling with unexpected medical bills or exploring rental finance tools, following CFPB’s insights can help you avoid hidden risks and safeguard your financial future.